Tax morality: The big shift in corporate tax attitudes

Once seen as best practice, minimizing tax and reporting profits in low tax jurisdictions is emerging as a corporate reputation issue. It’s not just the multinational giants – every business is now coming under greater scrutiny. Will companies take the lead on tax morality or is legislation the only way forward?

The late Australian businessman Kerry Packer once famously told a government inquiry: “I’m not evading tax in any way, shape or form. Of course, I am minimizing my tax. “If anybody in this country doesn’t minimize their tax, they want their heads read, because as a government, you’re not spending it that well that we should be donating extra.”

Mr Packer was hailed as a hero at the time. But 30 years on, the feeling of the general populace has shifted, and practices such as reporting profits in low tax jurisdictions is seen less as minimising tax and more as tax avoidance.

Increasingly, countries are complaining that they are missing out on US$427 billion from their coffers annually due to profits being reported in low-tax jurisdictions – and as awareness grows, tax morality is starting to emerge as a corporate reputation issue. Accusations that a company is a poor corporate tax citizen risks reputational damage in the community, and with investors and stakeholders, in the same mould of companies that refuse to shift on improving environmental, social and governance policies.

Androulla Soteri, Director of Tax at Baker Tilly International, says a shift in attitudes has resulted in scrutiny of what was once accepted as best practice. “Once, the general consensus was if we can avoid paying tax we will because it’s within the rules,” she says. “But over the last few years, companies have come under a lot of scrutiny for making very, very large profits, but not paying a commensurate amount of tax to the profits that they make. These mega-profits are widely publicised, we’re talking about Amazon, Google, those big household names, and that pressure flows over to all companies.”

Big multinational companies such as Apple, Microsoft and Google, are reported to have shifted as much as US$1.4 trillion in profits to low-tax jurisdictions such as the Cayman Islands, Bermuda and Ireland. “Every business is now coming under greater scrutiny of their record in terms of being ethical when it comes to the amount of tax that they’re paying, in relation to the activities and the resources that they drain,” Ms Soteri says. “What we’re seeing now is a move towards ethical tax policies, things like country-by-country reporting, that will force companies to declare how much tax they pay in each territory relative to their profit.”

Ines Paucksch, Global Leader Corporate Tax at Baker Tilly International, says companies are not giving away tax to governments but the aggressive tax planning of years past has vanished. “Companies still want to limit their tax liability and the tax ratio on their worldwide income is still an important KPI,” she says. “But they do want to pay it on a fair basis and for tax matters to be dealt with smoothly. It’s important for them as a company to accept social responsibility by looking at environmental impact, at the people working in the company, and at how and where they pay taxes. The spirit of companies has changed. They want to pay their fair share, it’s no longer a competition to do the most aggressive tax planning. It’s more to find the best compromise between paying taxes and the target of a low group tax ratio and I think that has changed in the last years.”

So will investors be prepared to walk away from companies not prepared to clearly outline their tax dealings, or will it come down to legislation to enforce transparency?

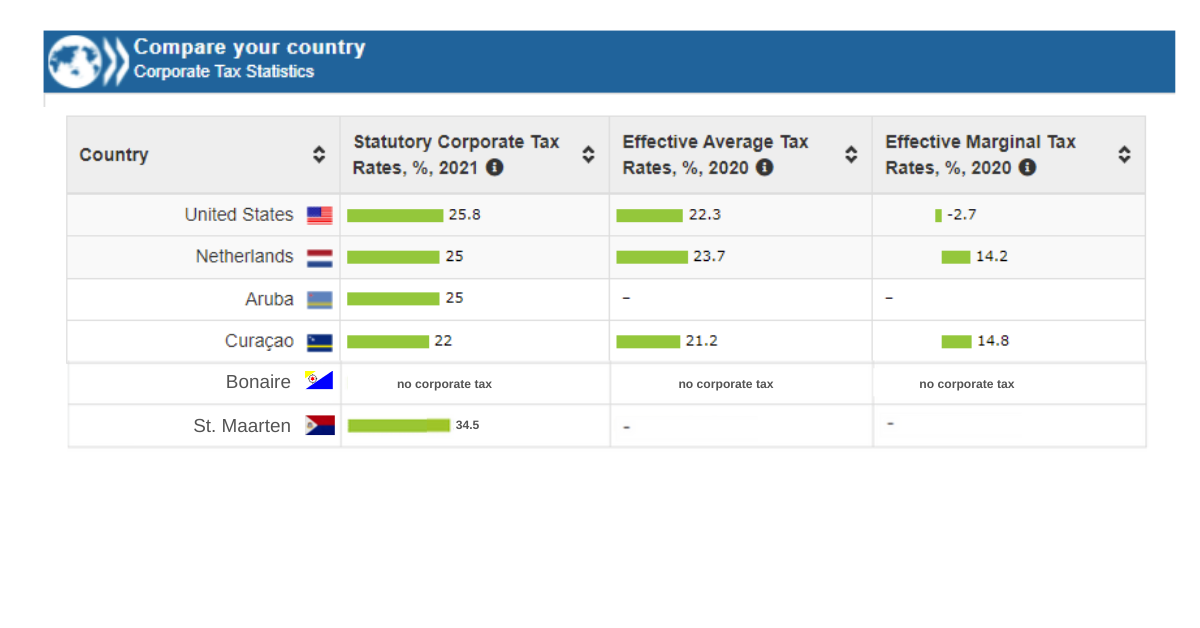

In the overview below we highlighted the comparison in the region when it comes to corporate tax rates:

The difficulty in legislating a global tax rate

Corporate tax is a delicate matter – directors are put in place by shareholders who seek a return on investments, and the companies use legal means to reduce the tax liability to improve those returns. Any changes to those structures may have an impact on shareholder returns.

On the other side of the coin, companies that are transparent about the jurisdictions where they are paying tax may indeed reduce the risk of reputational damage – but they also risk cutting into a competitive advantage, or falling further behind those who are comfortable with using tax havens to report profits.

In 1980, corporate tax rates around the world averaged about 40%, but as governments came to realize that lowering corporate tax could attract business investment, the average has come down and today it is closer to 24%, like Curacao (22%) and Aruba (25%). However, it still varies wildly between countries. Puerto Rico is one of the highest with 37.5%, St. Maarten at 34.5%, Brazil is at 34% and France 32%, while at the opposite end Barbados taxes companies at 5.5%, Hungary at 9%, Paraguay at 10% and Ireland at 12.5%. Countries with no corporate tax include Bonaire, the Bahamas, the Cayman Islands and Vanuatu.

Earlier this year, the European Union started moves to force multinational companies to publish a country-by-country breakdown of the tax they pay in each of the bloc’s member states, and in tax havens. And then there is the global minimum tax discussion. In July, the OECD hosted two days of talks where 130 countries, representing more than 90% of global GDP, backed an agreement for a tax rate of at least 15%. The minimum corporate tax does not require countries to set their rates at the agreed floor; instead, it gives other countries the right to apply a top-up levy to the minimum on a company’s income coming from a country that has a lower rate.

But the plan has met resistance from low-tax countries such as Ireland, prompting questions about whether an agreement can be reached. Ms Paucksch says there are several aspects to be considered. “Common taxes can be decreed with one consent only in the EU, we have to achieve unanimity where taxes are concerned,” she says.

“If some EU countries – Ireland, Estonia, Hungary – do not agree as they are looking for different business models, this has to be resolved. On the one hand, this could be achieved through political pressure. On the other hand, the relationship between the EU and the USA has to be taken into account. The USA might make an approval dependent on the further development of a digital tax in the EU. The introduction of a general digital tax in the EU was postponed until October. However, in countries like France the digital tax is already in place. The USA believes that the digital tax is aimed at US-based groups like Amazon, Apple, Google and Microsoft. They argue that these companies are taxed twice then – with the European digital tax and the worldwide pillars one and two approach. If the EU keeps its digital tax, the chances that US President Joe Biden can enforce the global minimum taxation in the congress may diminish.”

Ms Paucksch reiterated that the aggressive timeline being pursued was going to be difficult to meet, particularly in the midst of the COVID-19 pandemic. She says the upcoming G20 meeting in October will be interesting. “I’m really curious to see how things move forward and what we will learn in October at the next G20 meeting,” she says. “The participating nations committed themselves to implement the global minimum taxation in 2022 and putting it into effect in 2023. For just one nation this would be bold, but for a worldwide measure it is extremely ambitious.” While companies were recognizing the importance of paying their fair share of tax, Ms Paucksch says authorities need to be aware that the administrative burden on companies continues to grow. “The target can’t be that they spend more time in gathering the right data over everything else,” she says. “That’s a development that politicians and administrations should consider as well when they think about a new system of taxation, a new system for the future.”

Transparency can be the driving force for change

Even without legislation as the stick, Ms Soteri predicts that moral tax strategies will increasingly become a part of strategic tax planning, with companies not prepared to risk bad publicity over the issue. “I’d predict that in future, in terms of tax services, we’re going to have a lot more clients coming in saying to us, we want to have a moral tax policy,” she says.

“There’s an element of transparency, it’s a bit like the gender pay gap reporting. Authorities haven’t said you must make sure your employees are paid equally. They’ve said, be more transparent about what you’re paying, and the hope is that the issue resolves itself. So, country-by-country reporting has sort of been that same kind of principle. These companies want to be fully transparent and don’t ever want to be appearing in the headlines labeled as a company that isn’t paying a fair share of tax.”

Want to know more about corporate & global tax rates? Just contact our tax team;

Arthur van Aalst

vanaalst@bakertillycuracao.com

Anjli Finessi

Finessi@bakertillycuracao.com